The tide may be turning for tobacco stocks. After going through a 10-year period of zero returns -- including dividends -- British American Tobacco(NYSE: BTI) has posted a total return of 28% year to date. Investors are getting more bullish on the stock after the company called for a second-half acceleration of its business and strong organic revenue growth from 2026 onward due to greater contributions from its reduced-risk nicotine products.

Investors sitting on the sidelines have missed the boat on British American Tobacco's returns so far this year, but the party may just be getting started. Where will the stock trade five years from now? Time to investigate this nicotine giant and see if the stock is a buy.

Managing the combustibles decline

Investors have shied away from tobacco stocks in the last few years due to heavy volume declines in the United States. In 2022 and 2023, premium cigarette volumes declined 12% year over year, the worst two years of the 21st century. This even surpassed the volume declines during the Great Recession of 2008 and 2009.

As one of the largest tobacco companies in the country with brands like Newport and Camel, British American Tobacco has felt the brunt of this weakening consumer demand. Now, it looks like the market might be leveling off. Management says it is seeing signs of a recovery for the U.S. cigarette market, saying the low volumes were likely due to the high inflation of the last few years that has finally begun to wane.

Even though British American Tobacco's cigarette volumes are declining more than 10% annually in the U.S., the company's revenue is essentially flat over the last five years. It has been able to and likely will be able to continue implementing price hikes on cigarettes to counteract volume declines.

Second, it has exposure in foreign countries with better volume trends than the U.S. This dynamic should hold unless the bottom totally falls out from beneath the cigarette market here. British American Tobacco's combustible segment is likely to see flat revenue over the next five years too.

New products driving earnings growth

The combustibles business may not be as bad as people think, but it does not inspire much excitement for investors. Luckily, this isn't the only part of British American Tobacco's business. It also has products in the nicotine pouch, electronic nicotine vapor, and heat-not-burn tobacco device spaces. Its three brands are Velo (nicotine pouches), Vuse (vapor), and Glo (heat-not-burn).

Given the general trend of nicotine users switching from cigarettes to these alternatives, this segment has grown quickly for British American Tobacco over the last few years. Converting its British Pound currency to U.S. dollars, revenue for these new-age products has grown from $780 million in the first half of 2020 to $2.2 billion in the first half of 2024. With the added scale, the segment is now generating positive contribution profits and should contribute to bottom-line earnings growth.

These products are in more than 100 countries, so there is plenty of room left for growth. The segment can also counteract volume declines in the cigarette business, which is a big concern for investors. As this segment scales, investor fears over the collapse of the tobacco companies should slowly subside.

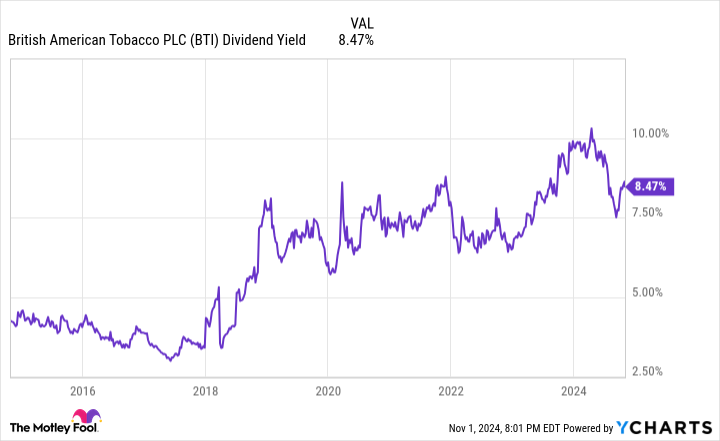

Data by YCharts.

Where will the stock be in five years?

Projecting the future for British American Tobacco requires making predictions for the future of its cigarette and new-age business segments. Assuming cigarette revenue remains flat in five years due to the competing dynamics of volume declines and price increases, new-age nicotine products will drive any growth on the top line. And I expect them to grow revenue by close to 10% annually for the next five years. There is a general sector tailwind here the company can tap into.

This may add up to around 3% to 5% annual revenue growth, which is exactly what management is expecting over the long term. If margins can expand as the new nicotine brands keep scaling, then earnings should be able to grow 5% to 7% per year over the next five years. As long as the stock trades at the same price-to-earnings ratio (P/E) in five years, this formula will equate to 5% to 7% annual stock price growth.

But this neglects something big: dividends. British American Tobacco currently pays out a dividend that yields 8.5%. Add this on top of the earnings growth and investors can get a total return of close to 15% over the next five years, maybe higher if management can grow its dividend per share each year. While the stock price may not rise at a rapid pace, investors can still generate strong returns by owning British American Tobacco stock over the next five years and collecting its large dividend payouts,

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $22,050!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $41,999!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $407,440!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 4, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool recommends British American Tobacco P.l.c. and recommends the following options: long January 2026 $40 calls on British American Tobacco and short January 2026 $40 puts on British American Tobacco. The Motley Fool has a disclosure policy.