There are many ways to invest in oil and gas, from upstream exploration and production (E&P) companies to midstream pipeline and infrastructure players, to downstream marketing and refining companies, to integrated majors that operate across the value chain.

The upstream side of the industry tends to be the most sensitive to changes in oil and gas prices. With oil prices near the lowest level in a year, even top E&Ps like ConocoPhillips(NYSE: COP) are hovering around their 52-week lows.

Here's why ConocoPhillips is an excellent dividend stock to buy now and can do well even if oil prices fall further.

Image source: Getty Images.

ConocoPhillips is thriving even amid lower oil prices

ConocoPhillips had a solid quarter, producing 1.917 million barrels of oil equivalent per day (boe/d), including record-high Lower 48 (continental U.S.) production of 1.147 million boe/d. Despite higher production, overall adjusted earnings were down 20% compared to the same quarter in 2023, and Lower 48 earnings were down 26.2%. The earnings decline makes sense given the average realized price in third-quarter 2024 was $54.18 per boe compared to $60.05 per boe in the third quarter of 2023.

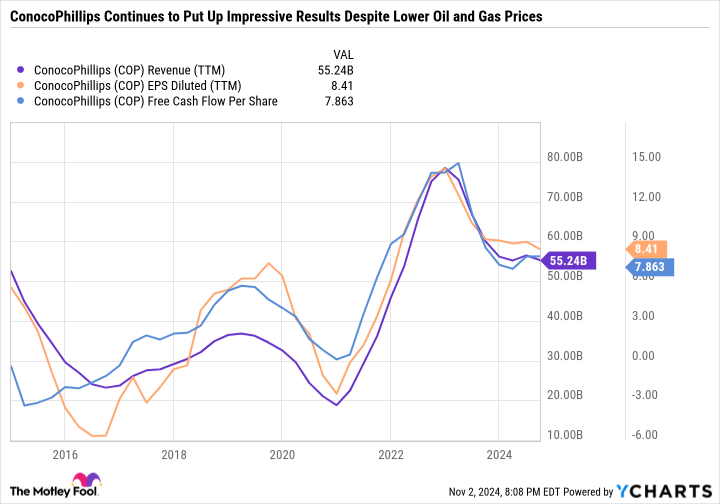

Still, ConocoPhillips continues to rake in plenty of earnings and free cash flow (FCF) to support existing operations and investments, and returning capital to shareholders. As you can see in the chart, ConocoPhillips' results have come down significantly from peak levels a couple of years ago, but it is still generating more sales, earnings, and FCF than it was pre-pandemic.

COP Revenue (TTM) data by YCharts

According to the Energy Information Administration data, West Texas Intermediate crude oil spot prices averaged $76.24 per barrel in the third quarter of 2024 (July to September) compared to $82.30 in the same period in 2023.

ConocoPhillips can deliver strong results even at mediocre oil and gas prices because it has gradually improved the quality of its asset base by prioritizing disciplined investing and focusing on assets with a low cost of production. On the earnings call, ConocoPhillips confirmed that its FCF breakeven is around the mid $30 per boe range, but it will decrease even further to the low $30 per boe range thanks to the synergies from the acquisition of fellow E&P Marathon Oil. ConocoPhillips said the dividend adds about $10 per boe to the breakeven level, meaning it can still achieve FCF breakeven and fund the dividend with cash at low $40s per boe.

Of course, ConocoPhillips needs oil prices to be higher than that to buy back stock and fund an aggressive capital spending program. But still, the low breakeven is a nice margin of error for risk-averse investors who want a company they can count on during industrywide downturns.

Improving an already excellent capital return program

When ConocoPhillips announced that it was buying Marathon Oil for an enterprise value (market cap plus debt) of $22.5 billion, it planned to buy back $20 billion in stock over the next three years to offset the shares issued for the transaction. In the first nine months of 2024, ConocoPhillips funded $8.8 billion in capital expenditures and investments, repurchased $3.5 billion in shares, and paid $2.7 billion in dividends. ConocoPhillips' pledge of $20 billion in buybacks in three years would look more like $1.7 billion in buybacks per quarter. But with the Marathon Oil acquisition expected to close in the current quarter, ConocoPhillips significantly updated its buyback and dividend plans.

For starters, it increased its existing share repurchase authorization by up to $20 billion, giving management the green light to buy back up to that amount before needing further board approval. On the earnings call, management said it plans to purchase close to $2 billion in stock in the fourth-quarter -- so the company is already showing signs of accelerating the buyback program.

ConocoPhillips is making a big change to its dividend program, which could leave more capital for buybacks and simplify the amount of passive income investors can except to collect from holding shares in the company. ConocoPhillips had been paying a mix of ordinary dividends and variable dividends based on the performance of the business. Now, it is getting rid of the variable dividend, or what it called a variable return on cash, and boosting the ordinary dividend by 34% to $0.78 per share -- giving ConocoPhillips a forward yield of 2.9%.

The company's ability to fund an attractive dividend while buying back stock at a breakneck rate is a testament to ConocoPhillips' strong asset portfolio and financial health.

ConocoPhillips' best days are ahead

ConocoPhillips remains the best all-around E&P to buy now. Marathon Oil should fit nicely into the broader portfolio and make the Lower 48 an even larger portion of total ConocoPhillips production.

Even at current oil prices, ConocoPhillips can buy back a considerable amount of stock and grow its already attractive dividend. And even if oil prices fall, income investors can rest easy knowing ConocoPhillips is a cash cow that can still fund its payout with cash during low-cycle environments.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $22,050!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $41,999!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $407,440!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 4, 2024

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.