Stocks that yield 4% or higher are particularly attractive, with the 10-year Treasury rate at 4.3% and the S&P 500 yielding just 1.5%.

A company's yield is nowhere near as safe as a return guaranteed by the U.S. government. However, investing in high-yield stocks is a simple way to unlock comparable passive income to the risk-free rate while also investing in the stock market. It's the best of both worlds -- so long as the company paying the high yield is a sound and growing business.

Here's why Chevron(NYSE: CVX), Diamondback Energy(NASDAQ: FANG), and Clearway Energy(NYSE: CWEN) stand out as three passive income plays to consider now.

Image source: Getty Images.

Chevron's cash isn't burning a hole in its pocket

Daniel Foelber (Chevron): Chevron is in the spotlight again, but this time, it's because its deal to acquire Hess may be in jeopardy. Chevron first announced the deal in October, which followed ExxonMobil's acquisition of Pioneer Natural Resources. The two deals spurred a wave of mergers and acquisitions, including Occidental Petroleum's deal to buy CrownRock, APA's acquisition of Callon Petroleum, and, most recently, the merger between Diamondback Energy and Endeavor Energy Resources.

Hess holds a 30% stake in the Stabroek block offshore Guyana. ExxonMobil and its partner CNOOC are claiming that Chevron's acquisition of Hess triggers a change in ownership, but Chevron argues it doesn't because it is acquiring an entire company, not just the Guyana stake.

Regardless of the outcome, the dispute will almost certainly delay the acquisition and act as an ongoing uncertainty for Chevron. The good news is the deal isn't necessary for Chevron to do very well.

The Hess deal was good but not great compared to Chevron's past deals. In the summer of 2020, Chevron was able to acquire Noble Energy during an unstable time in the industry. That deal was phenomenal in retrospect. Chevron also famously walked away from buying Anadarko Petroleum when it was outbid by Occidental Petroleum in 2019.

The main benefit of Hess was that it diversified Chevron's portfolio with access to Guyana, boosted its exposure to the Bakken basin, and included more minor positions worldwide, such as offshore from the Gulf of Mexico and Malaysia. Guyana has a low cost of production, but it also has geopolitical and development risks.

If the deal falls through, Chevron could simply accelerate capital expenditures in its existing portfolio, use the money to buy back its own stock at a great price (Chevron has a mere 13.4 price-to-earnings ratio), or pursue different acquisitions.

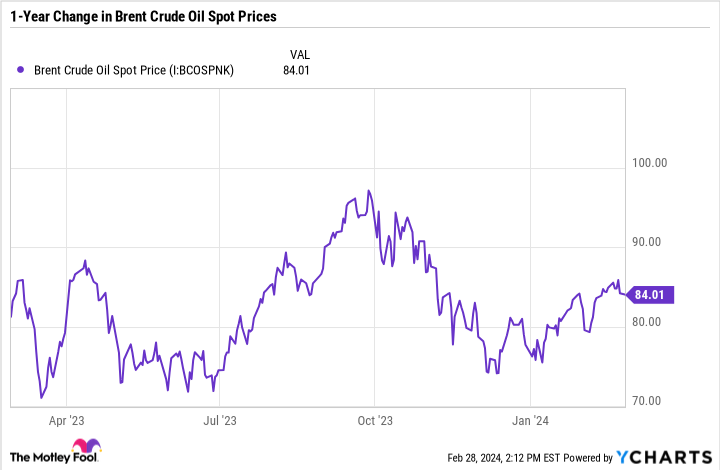

Since the deal was announced, Brent crude oil prices have fallen slightly. So, it's not like oil prices have run away from Chevron, and it is scrambling to catch up.

Brent Crude Oil Spot Price data by YCharts.

All told, Chevron should be in good shape no matter what happens. With a 4.1% dividend yield, the integrated major offers investors a sizable incentive to simply hold the stock through periods of volatility.

This energy stock is capable of paying huge dividends to investors

Lee Samaha(Diamondback Energy): Despite a slowing economy, the price of West Texas Intermediate crude oil (the U.S. benchmark) is still around $78 a barrel at the time of writing. While it's tough to predict the direction of the price of oil, demand will likely improve if and when interest rates decline.

Diamondback management hopes that's the case because it recently agreed to buy privately held Endeavour Energy Resources for around $26 billion in cash and stock.

The deal will add resources and transform Diamondback into the third-largest producer in the Permian basin. The deal is expected to close in the fourth quarter of 2024.

Even without the additional resources and cash flow from the deal, Diamondback is an attractive stock for income-seeking investors. The company pays a base and variable dividend. The base dividend, which now annualizes to $3.60, is protected down to a price of oil of $40 a barrel using hedging. Meanwhile, the variable dividend is paid out from the remaining cash flow alongside a policy of opportunistic share buybacks.

Ultimately, energy prices will lead Diamondback's earnings and cash flow, so investors should expect volatility in the variable dividend. Still, for reference, the $8.12 paid last year represents a 4.6% dividend yield. Alternatively, annualizing the $3.08 dividend paid for the fourth quarter of 2023 implies a 6.9% yield.

As such, Diamondback is an excellent way for income-seeking investors to get energy exposure.

Clearway Energy generates strong cash flow from its green energy assets

Scott Levine (Clearway Energy): Oftentimes, when income investors are considering energy stocks to supplement their passive income streams, it's with names that they've found in the oil patch. While it's a valid strategy, supercharging their holdings with renewable energy stocks, like Clearway Energy, is also a viable option. Clearway Energy operates a sizable portfolio of clean energy assets that generate strong, dependable cash flows, which the company then returns to investors in the form of dividends. After the company's recent reporting of its fourth-quarter 2023 financial results, today seems like a great time to click the buy button on this green energy powerhouse -- along with its 6.5% forward-yielding stock.

High-yielding stocks are great, but they mean little if the company is risking its financial well-being to satiate dividend-hungry investors. Fortunately for Clearway Energy investors, this isn't the case. The company generated $342 million in cash available for distribution (CAFD) -- a metric similar to operational cash flow -- and it paid out $311 million in dividends.

Looking ahead, management forecasts 2024 CAFD year-over-year growth of about 15% to $395 million due, in part, to the completion of several projects: Cedar Creek, Cedro Hill Repowering, and Rosamond Central Storage. With respect to the dividend, the company expects a hike of about 7% from $1.54 per share in 2023 to about $1.65 per share in 2024, or about $333 million -- an amount that will still be sufficiently covered by the CAFD if the company achieves its forecast. Beyond 2024, management expects to continue raising the dividend by 5% to 8% through 2026, supported by proceeds from the company's sale of its thermal business assets.

Should you invest $1,000 in Chevron right now?

Before you buy stock in Chevron, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Chevron wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 26, 2024

Daniel Foelber has no position in any of the stocks mentioned. Lee Samaha has no position in any of the stocks mentioned. Scott Levine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apa and Chevron. The Motley Fool recommends Pioneer Natural Resources. The Motley Fool has a disclosure policy.