The failures of SVB Financial's Silicon Valley Bank and First Republic Bank sent shockwaves through the financial sector. Investors feared contagion could spread across regional banks, leading to a sell-first, ask-questions-later mentality.

Amid this, one notable stock that has fallen about 25% since the beginning of March is Live Oak Bancshares(NYSE: LOB). Despite the setback, Live Oak Bank has established itself as a trusted partner for small businesses. Although the stock may have outpaced its true value amid its success with the Paycheck Protection Program (PPP) lending program, the current sell-off might offer an attractive buying opportunity.

The bank for small businesses got a big boost from pandemic relief programs

The U.S. Small Business Administration (SBA) sponsors lending programs to help small businesses refinance debt, purchase machinery, and build working capital. The 7(a) program is its most popular loan program, and Live Oak Bank is the top lender through the program. Live Oak Bank has made nearly $1.2 billion in 7 (a) loans this year, outpacing Huntington Bank ($891 million) and Newtek Small Business Finance ($814 million).

Its position as a top lender put it in a prime place when the U.S. government introduced the PPP as part of its pandemic relief efforts in March 2020. From 2020 to 2021, Live Oak's net income exploded from $60 million to $167 million, with the boost coming primarily from PPP loans. Its rapid short-term growth sent the stock up 1,219% off its pandemic lows.

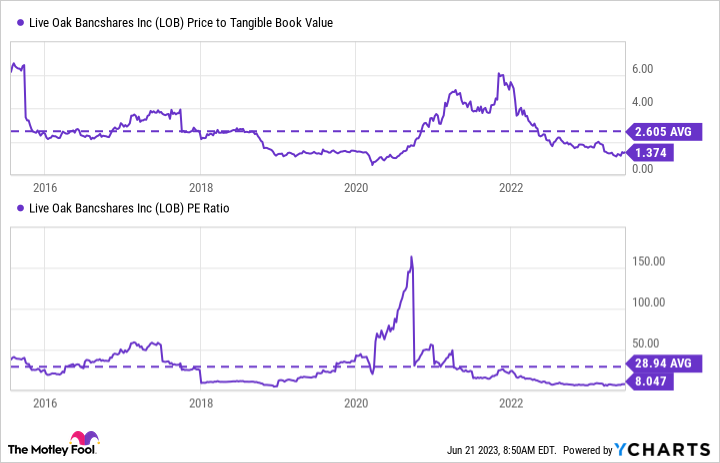

The explosive growth was short-lived, although the bank's earning rose 6% to $176 million last year. This was far from the rapid growth investors were pricing into the stock. In late 2022, Live Oak's stock reached a price to tangible book value of 6 -- more than twice as high as its 10-year average.

Image source: Getty Images.

Volatility in the banking sector and falling earnings have weighed on the stock

The failure of a Silicon Valley Bank and Signature Bank in March triggered a sell-off across the banking sector. These banks failed due to a combination of deposit outflows, which were largely uninsured, and large unrealized losses on the investment securities they held. It's worth noting that 85% of Live Oak's deposits are insured by the Federal Deposit Insurance Corp. In comparison, only 15% of Silicon Valley Bank's deposits were insured, giving depositor little reason to stay around when the bank's troubles surfaced.

If last year was disappointing for Live Oak, the first quarter was worse. Although the bank's interest income rose $59 million in the quarter to $151 million, that was mostly offset by a $54 million increase in interest expense. The bank also built up provisions to account for potential credit losses on its portfolio. This reduced its bottom line by over $17 million in the quarter. When all was said and done, Live Oak's net income plummeted from $35 million last year's first quarter to just $398,000.

Its valuation has plummeted

Live Oak's stock has sold off significantly. Since peaking at almost $100 per share, the stock has fallen nearly 75% and currently trades for less than $25 per share. Its price-to-earnings ratio is around 8, while its price to tangible book value is 1.4 -- about half its 10-year average.

Data source: YCharts

The cheap valuation makes Live Oak an appealing stock for investors to consider. The bank is on solid footing and saw deposits grow in Q1 at a time when many banks had deposit outflows. It also has enough liquidity to accommodate any potential outflows, with enough capital to cover 3 times the amount of its uninsured deposits.

It also holds high-quality loans on its books. Over 41% of its loans are guaranteed by the government, and many of them are in industries that have historically had lower defaults. And it has minimal exposure to office commercial real estate, a sector in trouble, given changes in people's work habits and higher refinancing costs.

A solid long-term buy

Live Oak Bancshares has carved out a niche serving small businesses. This focus benefited the bank in a big way when the PPP lending program was active but has since made year-over-year financial comparisons difficult, leading to a sharp repricing in the stock.

Live Oak has invested heavily in the Finxact core processing system, which allows it to be more agile and flexible in developing banking products for its customers. As a top SBA lender, these investments should allow it to attract more small businesses and serve its customers more profitably.

Live Oak stock has taken a beating over the past couple of years, but its cheap valuation makes this bank a solid buy today.

10 stocks we like better than Live Oak Bancshares

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Live Oak Bancshares wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of June 12, 2023

SVB Financial provides credit and banking services to The Motley Fool. Courtney Carlsen has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Live Oak Bancshares. The Motley Fool recommends SVB Financial. The Motley Fool has a disclosure policy.