Boeing(NYSE: BA) investors received some good news recently when the company released its delivery data for the first half of 2024. So what exactly was that news? And what could it all mean to an investment case for the stock? Let's dive in.

Boeing's delivery rates matter

Sales of commercial airplanes -- particularly its narrow-body 737s -- are the most important driver of Boeing's medium-term financial aspirations. The relative importance of its commercial airplane segment can be seen clearly in the medium-term financial plan Boeing management laid out in November 2022. Back then, management forecast that the company's free cash flow (FCF) would hit $10 billion in 2025 or 2026.

On a segmental level, the Boeing commercial airplanes (BCA) division is expected to do the bulk of the heavy lifting, delivering $9 billion in operating cash flow, while Boeing global services (BGS) is expected to deliver $3 billion and Boeing defense, space & security (BDS) $2 billion. (In case you are wondering why the numbers don't add to $10 billion, management expects $2 billion in cash taxes and another $2 billion will go on capital spending.)

Those targets for BCA's cash flow are based on management's assumption that the monthly production rate for 737s will hit 50, the rate for the wide-body 787 will reach 10, and the rate for the wide-body 777/777X will hit four.

A large part of Boeing's plan for profit margin expansion and FCF generation relies on the company ramping up production, which brings down unit costs. As production accelerates, assembly lines become more proficient and efficient as they get used to production processes.

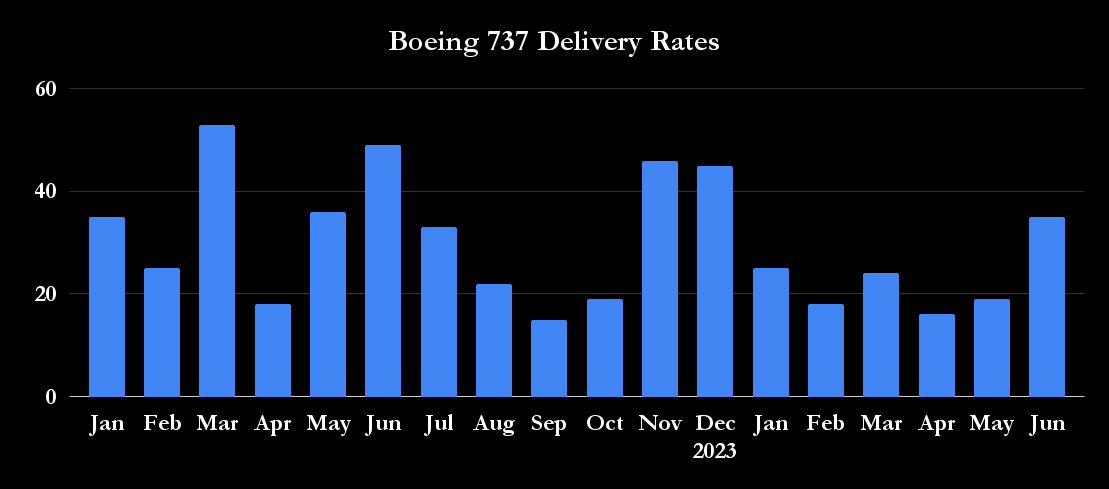

Boeing's delivery rates

Unfortunately, there are a few problems with that plan. First, Boeing has continued to suffer from high-profile production quality issues, which forced it to cut its production rates this year. This pushed back its production-ramping timeline and hindered its ability to improve profitability.

Image source: Getty Images.

Second, the variance in Boeing's delivery rates is also creating issues for its suppliers. While a slowdown on its part will help some suppliers catch up with its demand, it will put pressure on others. For example, on July 1, Boeing announced an agreement to acquire its fuselage supplier, Spirit AeroSystems, in an all-stock transaction.

While that's good news because it gives Boeing more control over its supply of fuselages, it's worth noting that Spirit laid off hundreds of workers early in the year in response to the slowdown in 737 production. Whether Spirit is a part of Boeing or not, the variance in aircraft production rates at Boeing is highly disruptive to Spirit's production plans.

Third, Boeing's 737 delivery rates have fallen behind schedule. It only made 67 deliveries in the first quarter (an average monthly rate of 22) and 70 in the second quarter (an average monthly rate of 23).

Here's the good news

That said, the 70 737s delivered in the second quarter included 35 delivered in June, as shown in the chart below.

Data sources: Boeing presentations. Chart by author.

Boeing's plans for 2024 involve getting to a delivery rate of 38 a month on the 737. Speaking at an investor conference in May, CFO Brian West said, "The first half, we had said, is going to be a production rate below 38 per month as we do the important work that I described, and then in the back half is where we're going to accelerate back toward the 38."

Clearly, by delivering 35 Boeing 737 airplanes in June, the company took a firm step toward the 38-a-month rate. While many of those 35 were likely airplanes that had already been in late stages of development and were therefore relatively easy to finally deliver, there were still processes that needed to be completed. The rising delivery rate is a good sign for Boeing investors.

What it means to investors

June's delivery ramp-up and the Spirit AeroSystems acquisition are steps in the right direction. All eyes will now be on the second-quarter earnings report Boeing will release at the end of July, in which management will provide updates about its production plans for the rest of the year. Investors will also want to hear how the acquisition of Spirit Aerosystems will help ensure 737 fuselage production rates can keep pace with Boeing's intended production pace.

While it looks as though the company's target of $10 billion in FCF in the 2025/2026 timeframe will be hard to achieve -- and management might even abandon that goal -- recent developments are positive. If the board announces a new CEO to replace David Calhoun (who is set to depart at the end of 2024), Boeing stock could recover through the rest of the year.

Should you invest $1,000 in Boeing right now?

Before you buy stock in Boeing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Boeing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $791,929!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 15, 2024

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.